THE 2025 yr is shaping up as a type of uncommon ‘goldilocks’ cycles within the beef business when all elements of the provision chain – cattle producers, lotfeeders and processors/exporters – get a share of the revenue margin pie.

Meat and livestock provide and demand, seasonal elements, processing capability enhancements and forex outlook all counsel that is doable.

The current previous has seen Australian beef margin share swing alarmingly from year-to-year, as herd measurement, climate situations, and different elements got here into play. Traditionally, each processors and producers have tended to make up for lengthy durations of loss-making with monetary ‘recharge’ durations, when margin is strongly of their favour.

The 2021-22 years noticed cattle costs hit unprecedented report highs, as processors and lotfeeders scrambled to safe feeder and slaughter inventory throughout herd rebuild. Flatback heavy feeders throughout a lot of 2022 traded in a variety round 550c/kg for lengthy durations, at one level pushing into the 600s, valuing a typical 450kg feeder steer at $2700. Processors racked up huge losses through the interval because of this, whereas many producers, blessed with good seasonal situations, stacked up cash like King Solomon.

However two years earlier throughout 2019, it was beef processors making a killing (each metaphorically and figuratively talking – pun supposed) with plentiful, comparatively low-cost cattle on account of herd liquidation, coupled with vigorous export buyer demand, particularly in ‘new frontiers’ like China.

Even final yr, lotfeeders had a discipline day from mid-August by to early December, with feeder steer costs collapsing by 100c/kg to as little as 200c/kg, as producers panicked within the face of dry situations and a miserable BOM summer time seasonal outlook on the time. Younger cattle took the same path, with the EYCI falling 200c/kg (dressed weight equal) between late August and mid-October.

However some uncertainty surrounding subsequent yr’s demand and provide throughout some international protein markets, there’s trigger to suspect that the Australian business revenue margin pie will probably be divided far more equitably over the following 12 months.

Right here’s some explanation why:

Season:

Seasonally, the outlook for subsequent yr is now quite a bit higher than it was even a month or two in the past – particularly in southern elements of the nation, organising the early a part of 2025 with some confidence.

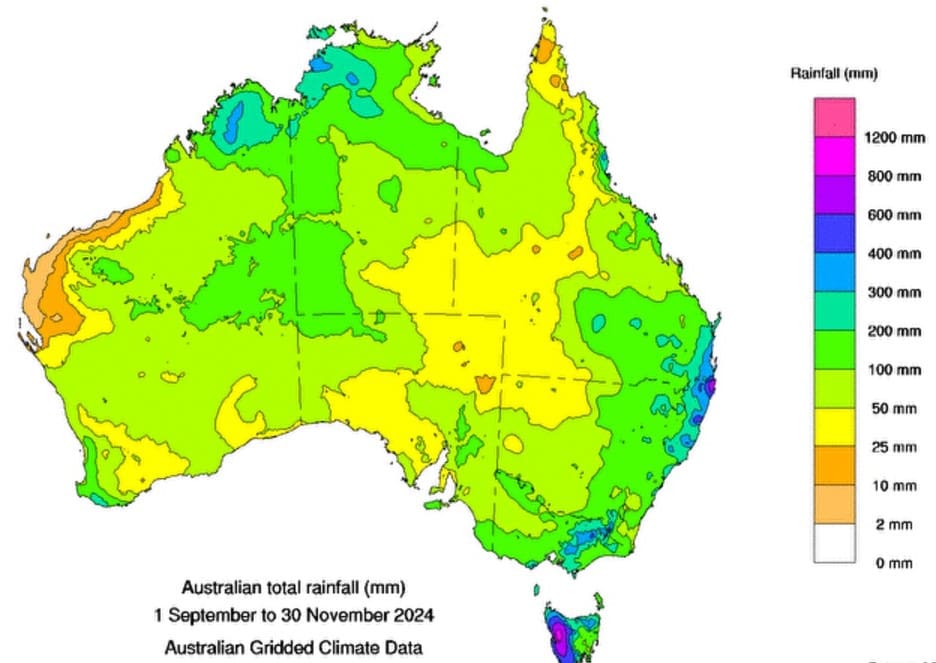

As proven on this BOM map of rainfall over the previous three months to the tip of November, massive areas of japanese Australia have now had a great begin to the summer time season, with falls of 100-+200mm widespread throughout japanese elements of Queensland, NSW and Victoria over the previous three months. December falls acquired over the previous three weeks will solely add to that. The Southern Oscillation Index presently sits at +7, near its highest level all yr.

Foreign money:

The Aussie greenback (measured towards the US buck) sat yesterday morning at US62c – its lowest level all yr, and actually since March 2020, when distortions created by COVID had been buffeting forex. A low A$ provides to Australia’s beef export competitiveness in worldwide markets.

Processing capability:

Labour provide challenges noticed beef processors tap-out at weekly kills (NLRS numbers) round 145,000 head throughout 2024 – however that solely got here within the latter phases of the yr, as labour numbers progressively constructed. Supporting that, the fourth quarter of 2024 ending 31 December guarantees to be the biggest quarterly nationwide slaughter quantity since September, 2015.

Analyst Simon Quilty believes that subsequent yr, capability to course of cattle will develop a bit of additional, to a determine presumably round 155,000 head – a seven p.c rise on this yr’s peak numbers – as new capability comes on-line and extra workforce is added at different websites.

Barring widespread drought, that ought to assist insulate towards danger of cattle value distortion brought on by numbers backing-up an excessive amount of, ready for a kill slot in under-manned vegetation. And with respectable margins on supply in processing subsequent yr, processors will once more be motivated to construct on present workforces.

Cattle value stability:

Australian younger cattle and completed steer costs had been remarkably secure throughout 2024, and are prone to proceed so subsequent yr. Completed steer costs in 2024 traded inside a comparatively slim band of 120¢/kg (carcase weight) since January, and have traded inside a 70c/kg band from 550–620¢ since July.

The maturation of Australia’s herd rebuild right into a constant provide of slaughter-ready cattle, when paired with rising processor capability and rising demand in export markets, has allowed costs to stay regular over the yr, in marked distinction with excessive value volatility seen in 2023.

Younger cattle are the identical – the EYCI has been remarkably secure by 2024 – buying and selling in a 150c/kg band from 541c/kg (dw equal) to 692c. Examine that with the 2023 yr, when common weekly costs ranged from 785c to 349c – a diffusion of just about 440c.

Cattle provide:

MLA’s newest business projections forecast has the nationwide cattle herd at 29.57 million head subsequent yr, down 2pc on this yr as a result of gentle destock that’s occurred in elements of southern Australia on account of dry situations.

MLA forecasts slaughter numbers subsequent yr at 8.38 million, up 200,000 head or 2.4pc from this yr. Offsetting that, carcase weights are forecast to say no 5kg to 305kg. Beef exports subsequent yr are forecast to carry one other 17,000t to a report 1.904mt.

The nationwide cattle herd has reached and handed a cyclical peak after working at maturity for the previous 12 months. Elevated turn-off will guarantee a better provide of completed beef, although turn-off of retained and utilised cows will stabilise the breeding herd, MLA says.

The northern herd is anticipated to stabilise into 2025 as average-to-good moist seasons will proceed to assist a big, productive breeding herd and rising numbers of cattle exported into South-East Asia.

The southern zone has skilled some contraction within the again half of this yr, as sturdy abroad beef demand helps increased turn-off in a now-mature herd.

Slaughter is anticipated to rise above ten-year averages, however stay effectively under the all-time peak beforehand set throughout drought turnoff in 2014.

If seasonal situations stay largely common in southern Australia and average-to-good in northern Australia, MLA means that will increase in turnoff will probably be pushed by rising availability of processor-ready cattle, versus a climate-driven want to cut back stocking charges.

Particularly, a lot of the breeding herd that was retained to energy the rebuild is now mature and able to be turned off.

“We count on that a lot of the rise in slaughter will probably be from this cohort, which is able to push the feminine slaughter fee above common. This dynamic has been evident throughout the primary two quarters of 2024 and can proceed,” MLA stated.

Export clients: US manufacturing descending

Australian lean beef trimmings offered frozen into america hit a report excessive of 1024c/kg final week, because the influence of US herd liquidation begins to take full impact.

The fundamental driver is the big decline being seen in US non-fed slaughter, on account of the influence of drought and herd decline.

Fed cattle (ie steers and heifers completed in feedlots) slaughter within the US this yr has remained surprisingly excessive, regardless of the nationwide beef herd declining to 50-year lows on account of drought liquidation.

For the week ending 7 December, complete US cattle slaughter was 614,000 head, representing only a 3.8pc year-on-year decline. Fed cattle slaughter was regular at 495,000 head, however crucially, cow/bull slaughter (nearer aligned with manufacturing meat) dropped 17pc in comparison with final yr, and 24pc in comparison with two years in the past.

“US packers are struggling to safe enough cattle for manufacturing regardless of feedlot inventories matching year-ago ranges,” analyst Len Steiner stated a fortnight in the past.

US packer margins continued to deteriorate on account of excessive cattle costs. Tyson Meals’ current choice to shut a meat processing plant mirrored broader considerations about tightening US cattle provide.

“Additional reductions in US cattle processing capability could also be inevitable as packers alter to projected provide tendencies over the following three years,” Mr Steiner stated.

US manufacturing falling

In its 16 December Livestock Outlook report, USDA stated US beef manufacturing subsequent yr is forecast to fall by 1370 million kilos or 5pc, on present yr quantity.

Consequently, US beef imports are forecast to rise by 122 million kilos, or 3pc.

US cattle costs (Steers 5-State space direct) are forecast to rise even additional to US$191/cwt, up 10pc on two years in the past, USDA suggests, whereas feeder steers are forecast to extend one other 8pc.

As a result of fewer feeder cattle are anticipated to be positioned on feed heading into 2025, there are anticipated to be fewer slaughter steers accessible for processing beginning in second-quarter 2025, and persevering with for the following yr or two.

Including to the cattle dynamic is the current discovery of New World Screwworm in cattle in Mexico and the following US import ban on cattle from or transiting Mexico. The ban is assumed to stay in place till the coverage modifications, which is anticipated to restrict accessible slaughter cattle beginning in second-quarter 2025.

Export opponents: US

For a similar causes described above, the US is shaping as much as be a a lot much less vigorous beef export competitor for Australia in 2025.

US beef exports are forecast to fall by 365 million kilos or 12pc subsequent yr, affecting key markets like Japan, South Korea and China. Value of manufacturing rises within the US as slaughter cattle grow to be more and more scarce will even problem US competitiveness in markets the place we each compete.

Export opponents: Brazil

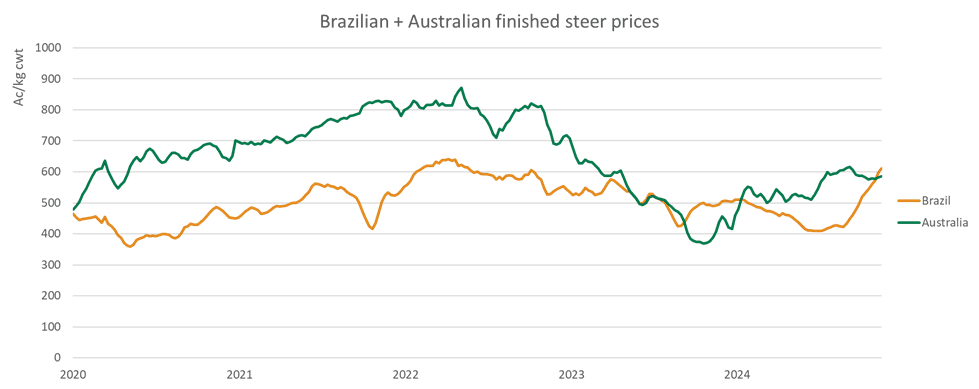

Brazilian processor steer costs have risen 52pc since June, which means Australian cattle in early December had been barely cheaper than equal Brazilian cattle in A$ phrases (see graph).

The sharp rise in Brazilian cattle costs can broadly be attributed to a slowdown in provide. After a number of years of drought situations driving cattle slaughter up, provide of completed cattle has begun to tighten and Brazilian slaughter has begun to decelerate. When mixed with comparatively constant export demand, this has pushed up demand for present slaughter-ready cattle.

Provisional November month-to-month slaughter at 2.13 million head had been 5pc under October 2024. Whereas nonetheless very excessive, that is the primary time slaughter has been under year-ago ranges since 2021 and marks the fourth month of constant declines in Brazilian slaughter.

The rise in Brazilian costs makes Brazilian beef considerably much less aggressive in export markets, and acts as a sign of tightening provide. The markets the place Brazil exports essentially the most beef are usually comparatively price-sensitive (ie China), so elevated prices are prone to correspond with decrease exports over time, analysts counsel.

Indicators of tighter provide and margins for processors in Brazil got here in a current report from World Agritrends, which stated Brazil’s JBS deliberate to close down at the very least 11 of its South American processing vegetation in December and had suspended gross sales to China. There was unofficial reviews that there is likely to be as a lot as 15 factories. A number of smaller Brazilian meat packers had been stated to be following swimsuit.

A surge in dwell cattle costs in Brazil was cited because the set off for the shutdown. In current months, Brazilian dwell cattle costs have risen by a 52pc, far exceeding business expectations, World Agritrends wrote. This prompted the manufacturing prices of meat firms like JBS to extend considerably, and their revenue margins had been severely compressed. The businesses finally needed to cease manufacturing to deal with the difficulties, the service stated.

“With beef inventory inside China falling within the final six months, this fall in Brazilian exports is prone to see freezers in China emptied additional and costs enhance throughout beef, sheepmeat and rooster,” World Agritrends wrote.

“With rising costs in China, additional beef is prone to be diverted away from the US market, which can also be value supportive for US imported grinding meat costs.”

Confidence

Market confidence has actually shifted throughout 2024 from final yr – many would say final yr was the primary time in a very long time that producers decided based mostly on a forecast fairly than precise climate occasions. This confidence influenced shopping for behaviour; nonetheless, regardless of poor situations in Victoria and SA, costs remained sturdy on account of demand from NSW and Queensland producers.

All eyes have been on the worldwide market, notably america, which has recorded the bottom cattle herd in about 70 years. This has pushed excessive cattle costs and thus elevated the quantity exported.

“Sure there could also be emergence of improved confidence in Queensland within the latter half of 2024, nevertheless it’s a really good distance in each financial and cattle cycle phrases from the place we had been in 2022,” Stonex livestock and commodities supervisor Ripley Atkinson stated in his most up-to-date weekly bulletin.

“Confidence is king in at the moment’s markets, for each cattle and sheep, and it’ll stay a key theme to look at intently in 2025 as to what sort of affect it has on the course of the market,” he stated.

Stability

One other a part of the ‘confidence’ story heading into 2025 is stability.

No doubt, the cattle market has stabilised in 2024 – reflecting the balancing act between provide and demand that are influenced by climate, general confidence and elevated feminine slaughter, amongst many different elements.

Costs during the last 12 months have lifted by 20–40pc, indicating the restoration of the market from the difficult situations in 2023.

Trending Merchandise